Dear Client,

We are hoping this update finds you and your loved ones doing well as we say goodbye to an unusually mild winter and welcome in new growth with the many treasures of Spring. Along the lines of growth, we have continued to see the markets grind forward with the momentum which began last year. For the first quarter most equity indexes provided anywhere from 5%-10% growth, and bond yields remained strong as well providing north of 5% annualized income in most cases.

Economy

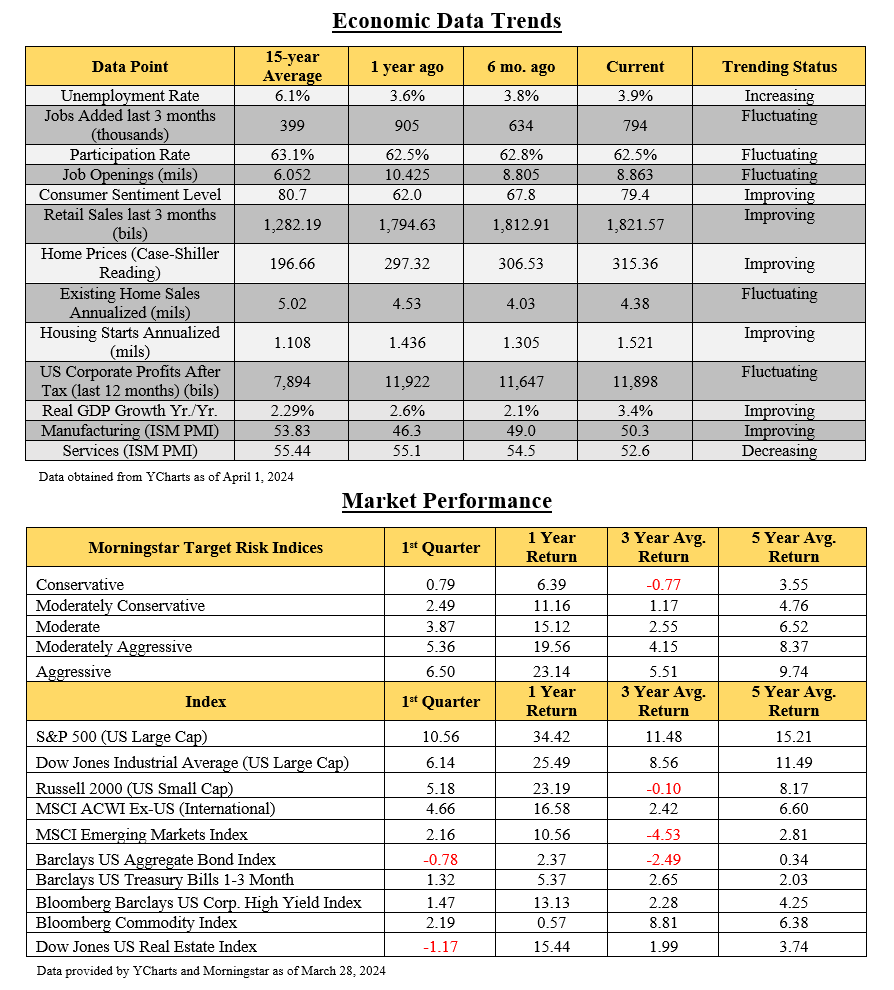

While the Fed has failed to meet their stated 2% inflation objective, they have achieved a significant reduction from 9% to the 3%-4% range, which is far more manageable for most consumers. Although some original estimates predicted 6 rate cuts during this year, the Federal Reserve has since indicated a likelihood of only 2-3 in 2024, the first of which will not likely occur until June or possibly even later. While it seems lowering rates would be good, the reason they are not may be even better. Earlier in the year the assumption was that we would see a softening of the economy, whereby lowering rates would be necessary to facilitate a “soft landing.” The good news (or bad news depending on your perspective) is that the economy has shown unexpected resiliency over the first quarter, which may continue throughout 2024.

Last month the Conference Board’s Leading Economic Index (LEI) increased for the first time in over two years. While unemployment has moved up slightly, it is still below 4% and there are more job openings than there are people willing to fill them. The manufacturing index increased to its highest level in almost two years. Housing activity and home values have remained strong when compared with long term historical averages. Consumer Sentiment has grown significantly over the last year, and retail sales have also remained strong. Corporate profitability and strong earnings reports have also provided a boost to investor confidence and the ongoing surge we’ve seen in the markets.

With all that said, up to this point the Fed has balked on lowering rates due to stronger economic data than expected, which investors have perceived as a positive looking forward. If we do begin to experience a softening of the economy, the Fed now has a tool in their toolbox to lower rates and help fuel growth through monetary easing. However, lowering rates could be received with mixed emotions by investors, and it doesn’t necessarily mean they will respond with the type of exuberance we have seen recently. In fact, historically if the Fed is required to conduct a series of rate cuts, the market has typically responded unfavorably, seeing it as a sign of economic weakness.

Markets

Although we are at, or near, all-time highs on many equity indexes, this is not necessarily a signal of a correction on the near-term horizon. Investor confidence and market momentum have both remained strong through the first quarter, and as mentioned in our last update, the market historically does well during presidential election years. However, based on the many economic factors outlined above, along with current market conditions, we believe a strategic approach with tactical allocations is more important than ever.

Currently valuations in certain styles and sectors of the market are stretched well beyond their historical norms. Within the Legacy Portfolios we are allocated to manage our exposure in these categories and optimize the portfolio on an ongoing basis to protect our downside exposure. Simultaneously, we are allocating to sectors and styles that are fairly valued, or even undervalued, to benefit from these market inefficiencies.

We’ve continued to see strong performance in our alternative strategies, equity, and fixed income holdings when compared to the appropriate indexes and blended benchmarks. Accordingly, we are maintaining our current manager lineup and will continue to exercise rebalancing as appropriate, and tax loss harvesting as available within your Legacy Portfolio.

Asset Allocation Comparative

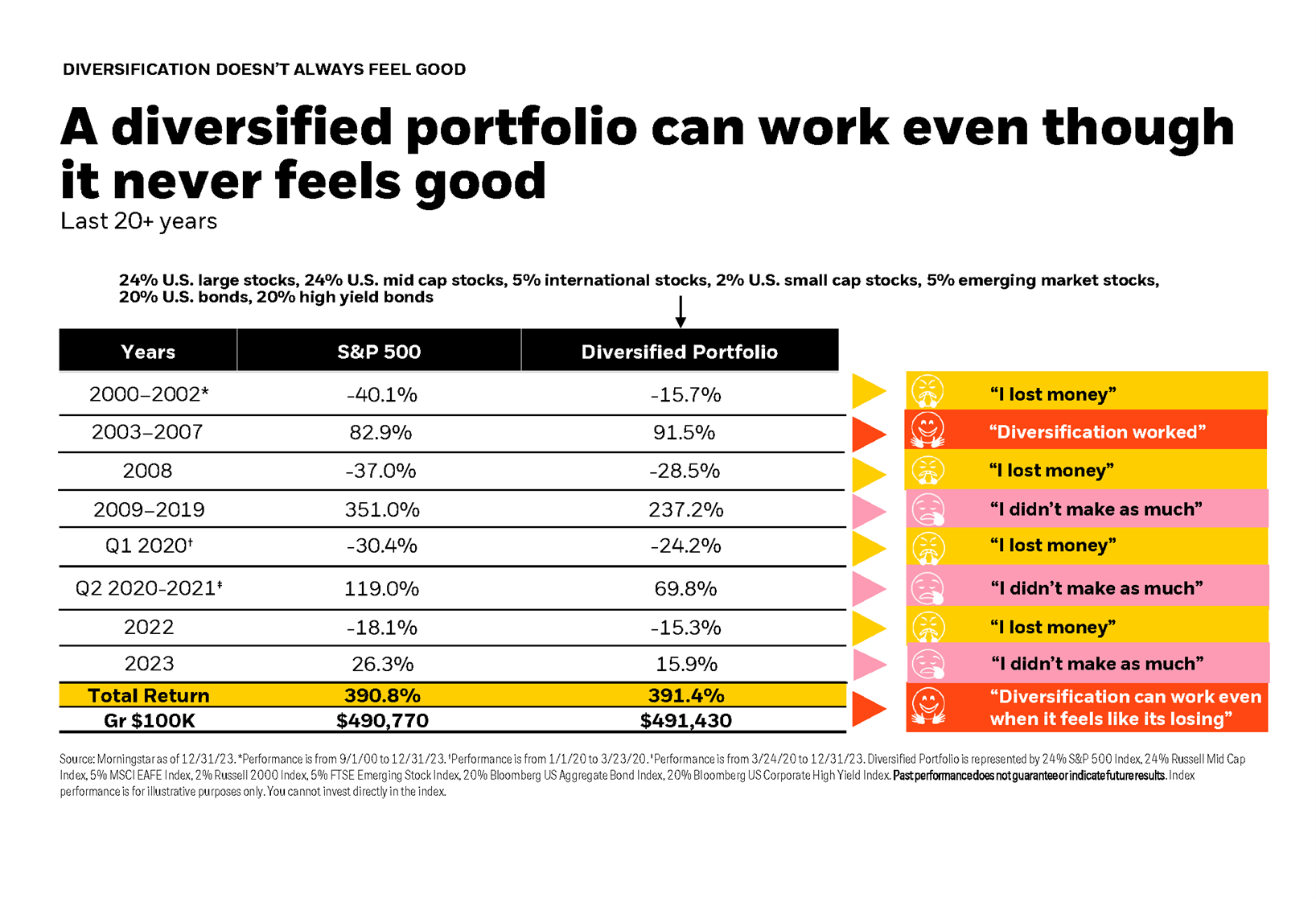

We are not recommending a change to your overall asset allocation. Instead, we want to provide an affirmation that your investment mix should remain optimized in alignment with your planning objectives and risk assessments. The tendency when markets go up or down significantly is to second guess a prudent approach and create an emotional roller coaster that we want to help our clients avoid.

The following table compares the journey of an investor when comparing a portfolio invested 100% in the S&P 500 vs a far more conservatively allocated portfolio with 60% in equities and 40% in bonds. While this isn’t a recommendation for either type of allocation, as your specific allocation should be in alignment with your unique circumstances, it tells a compelling story pertaining to the benefits of diversification during volatile cycles.

Please take some time to review the enclosed update of your portfolio, along with the Privacy Statement and update of our ADV form which we provide each year. Should you have questions or concerns regarding your current planning, portfolio, or anything else we can help with, please let us know. As always, we consider it an honor and a privilege to be able to help you with your wealth management and look forward to doing so for many years to come.

Kindest regards,

Michael Brocker

MSFS, CLU, ChFC, AEP®, AIF®

Chartered Financial Consultant

Masters of Science in Financial Services

Matthew Brocker

MSFS, AEP®, RICP®, CAP®, AIF®

Masters of Science in Financial Services

Josh Brocker

CFP®, AIF®