Dear Client,

We hope this update finds you and yours enjoying the first movements of this symphony we call Spring. Living in Minnesota all my life, I’ve noticed there always seems to be a genuinely optimistic outlook for what lies ahead, knowing most of the worst is behind us. We are currently embracing a similar type of cautious optimism as it pertains to the geopolitical conflicts we have experienced and our longer-term outlook.

Economy

As you have likely experienced at the pump, the war in the Middle East has provided a great deal of turbulence in the energy markets, more specifically with oil and gas. We’ve seen major daily price swings during the last few months, with the price per barrel of Brent crude ranging from lows around $60 to highs around $120 over the quarter. The hope is that if the Strait of Hormuz is secured, oil prices will come back down to more reasonable levels. Futures markets would indicate that most investors believe this will be the case. In the near term, higher energy prices are clearly having a negative short-term effect on the economy. The hope had by all is that a solution is forthcoming and the adverse impact will be short lived.

Amid this uncertainty, and the potential longer-term impact it will have on the economy, we have seen some economists pull back on their projections for economic growth (GDP) for 2026. We’ve also seen some economists harboring a sentiment for heightened recessionary risk if a favorable outcome is not achieved in the near term. Although things are changing daily, the uncertainty surrounding the true impact continues to linger.

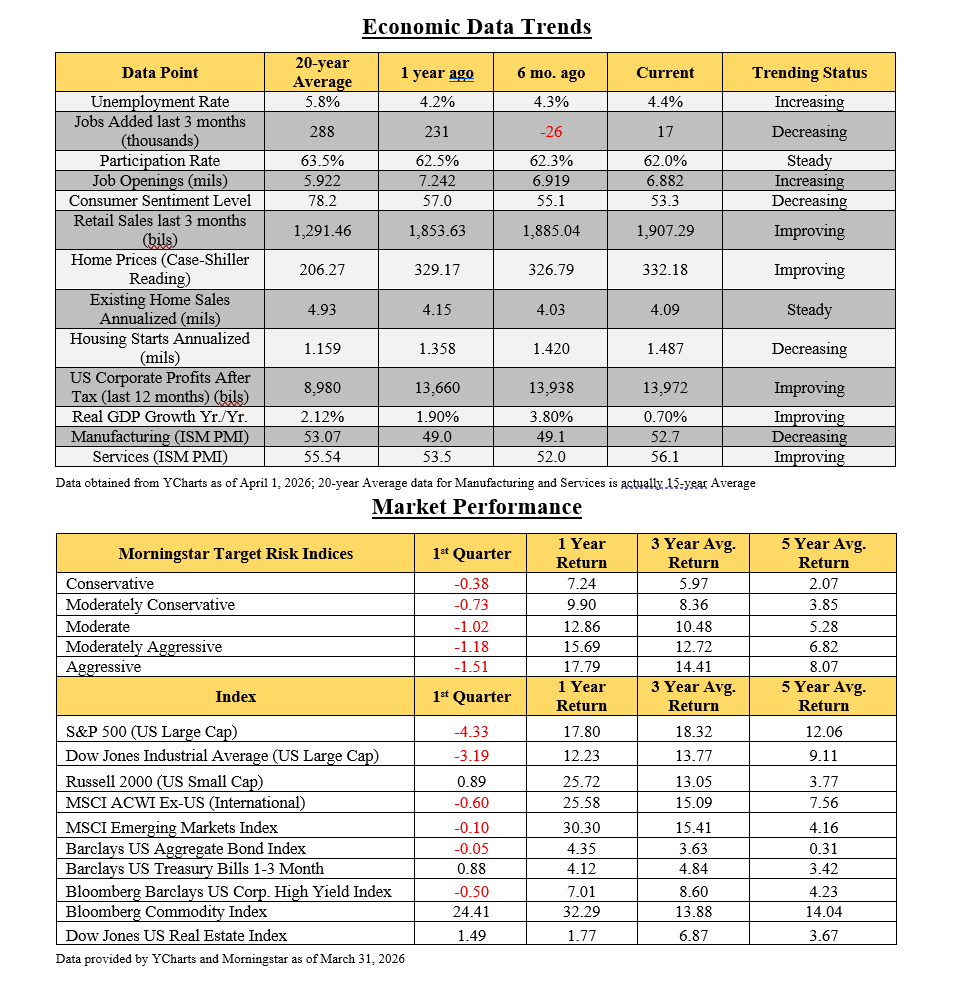

With that said, it has been encouraging to see continued resiliency in the US economy thus far. As you’ll see in the updated figures, many indicators pertaining to employment, housing, productivity and profitability remain strong relative to their longer-term averages. It’s important to also note that although there is a sentiment of increased risk of recession by some, there are also many analysts and economists projecting both strong economic and market growth once this is behind us.

Markets

We’ve seen another quarter with levels of market fluctuation that has far surpassed the average. Although this type of volatility is to be expected during heightened times of uncertainty and geopolitical unrest, we want to avoid getting too close to the daily gyrations. While a couple of indices did hit correction territory during the quarter, equity valuations as measured by PE ratios have improved, and the underlying fundamentals on much of the market remains strong.

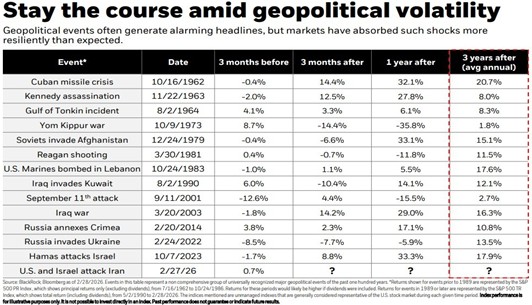

As shown in the table to the left, market volatility due to global unrest is not a new phenomenon. These periods can create uncertain near-term outcomes as evidenced by the column showing market results ‘3 months after’ or even ‘1 year after’. However, when considering an expanded horizon, stocks have shown buoyancy against event driven cycles.

Over the quarter we have also seen a shift whereby active management strategies are once again being rewarded. Emphasizing reasonable valuations, solid fundamentals and broad diversification has helped mitigate the downside we are seeing within the tech heavy exposures in the S&P and NASDAQ specifically. As the long-predicted market rotation and broader dispersion begins to play out we continue to believe proper diversification and thoughtful security selection will help us continue to effectively manage downside market volatility while providing strong long term growth potential moving forward.

Portfolio

As referenced above, although we did see significant volatility and an overall pullback in the broader markets, your diversification helped us mitigate some of that downside thus far, while still keeping us well positioned for future growth. Additionally, with the concerns some economists have over the risk of stagnant economic growth paired with higher inflation (stagflation), we believe it lends credence to maintaining broadly diversified holdings in the portfolio.

We have continued to engage in rebalancing within your portfolio as appropriate, to maintain the proper overall allocation based on your planning needs and objectives. We also continue to monitor opportunities for tax loss harvesting to help decrease capital gain exposure when it makes sense to do so.

After a more challenging year for active managers in 2025, we have been pleased to see the majority of our portfolio managers outperforming their relative benchmarks and overall portfolio performance holding slightly above the blended benchmarks.

Please take some time to review your customized portfolio review enclosed. Should you have any questions, concerns, or any changes to your overall financial objectives, please let us know. As always, we consider it an honor and privilege working with you and look forward to helping you and your family with your financial goals and concerns for many years to come.

Kindest regards,

Michael Brocker

MSFS, CLU, ChFC, AEP®, AIF®

Chartered Financial Consultant

Masters of Science in Financial Services

Matthew Brocker

MSFS, AEP®, RICP®, CAP®, AIF®

Masters of Science in Financial Services

Josh Brocker

CFP®, AIF®