Dear Client,

We hope this update finds you and yours celebrating a wonderful 2025 and looking forward to 2026 with great hope and anticipation for all that is ahead. We are coming out of what could be one of the most eventful years on record since I began my career almost 40 years ago. It has been encouraging to see the economy and the markets maintain a remarkable and almost inexplicable level of resilience, pushing most market indices to double digit returns for the year, while at the same time doing so in ways that call for even greater thoughtfulness and intentionality as we look ahead.

Economy

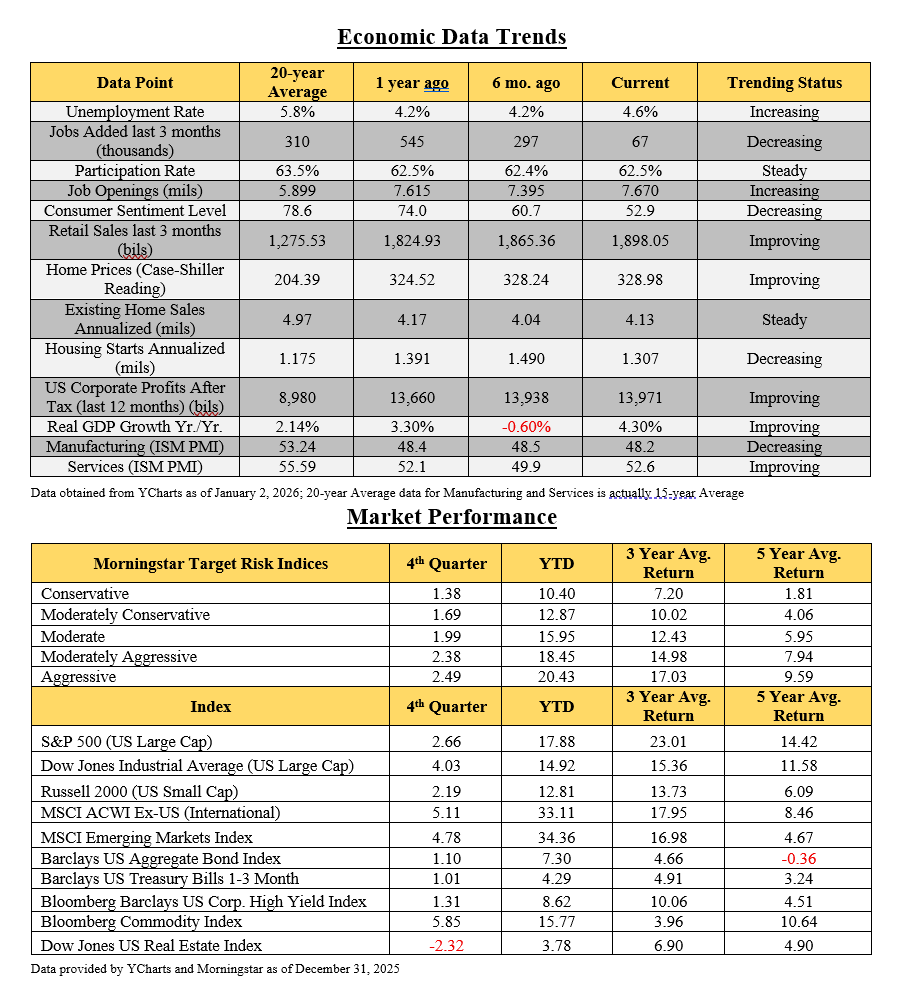

Amid global unrest, government shutdowns, new tax legislation, Fed rate cuts, sticky inflation, exuberant AI investing, and trade/tariff concerns that drove markets into bear territory back in April, the economy has remained relatively strong. As you’ll see in the enclosed report, unemployment, job openings and consumer sentiment are all moving mildly in the wrong direction, while retail sales, home sales, manufacturing, and GDP are moving on a more positive course. As always multiple factors will play into the economic outcomes we will experience.

While inflation has been held in check most recently, there are still concerns over the longer-term inflationary pressures we may experience due to tariffs, most of which will play out over the next 12-18 months. New tax cuts should help boost GDP due to greater consumer spending in the first quarter, and there is hope that this along with other growth initiatives from the current administration will invite a new “Golden Era” for the US economy. While the optimism is encouraging, we need to keep in mind that these initiatives are coming into play amid frothy equity markets and tech/AI investing that is pushing valuations and overall market share to levels that question the sustainability of those valuations.

Markets

As mentioned, the markets have continued to grind higher, which we have seen before. The following graph is from the end of last quarter, and the theme continued to play out through the end of the year. It illustrates the levels of growth we have seen from tech companies with no revenue or profits, compared to profitable companies, which are typically solid companies with good balance sheets and strong management. While historically these types of companies are logically rewarded with stronger returns, the new “risk on” phase created a very different outcome in 2025.

This uniquely divided market echoes some of the same themes we saw going back a quarter century to the late 90’s when dot-com and internet companies with no revenues or profits were providing exponential returns, while higher quality companies underperformed.

The caution here is in understanding what happened to the overcharged segments of the market when sanity returned. Although we don’t know when or if a similar correction may occur, we want to be exceedingly cautious with our investing strategy to avoid excessive exposure to areas that may be positioned for larger downturns if/when they occur. Not only so, but we also want to prioritize your long-term growth moving forward, which we believe we are well positioned to do in line with your longer-term planning objectives.

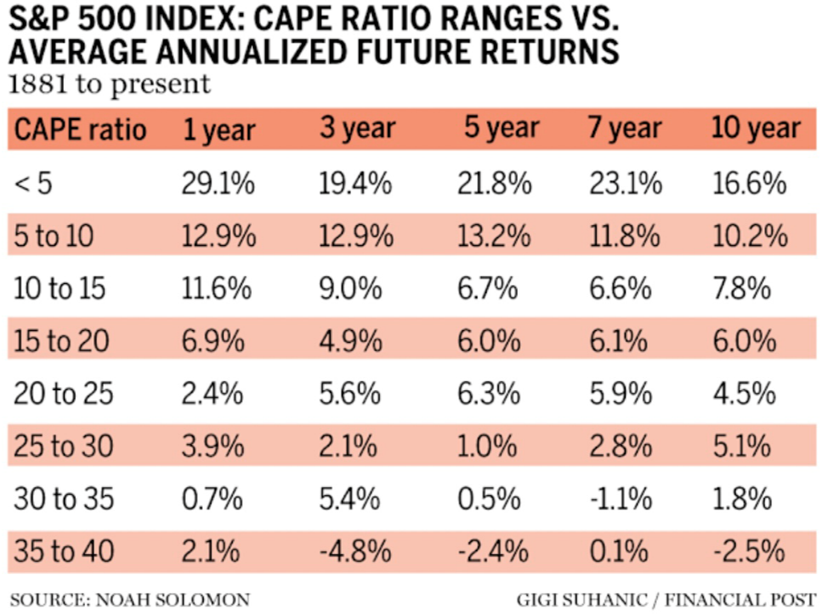

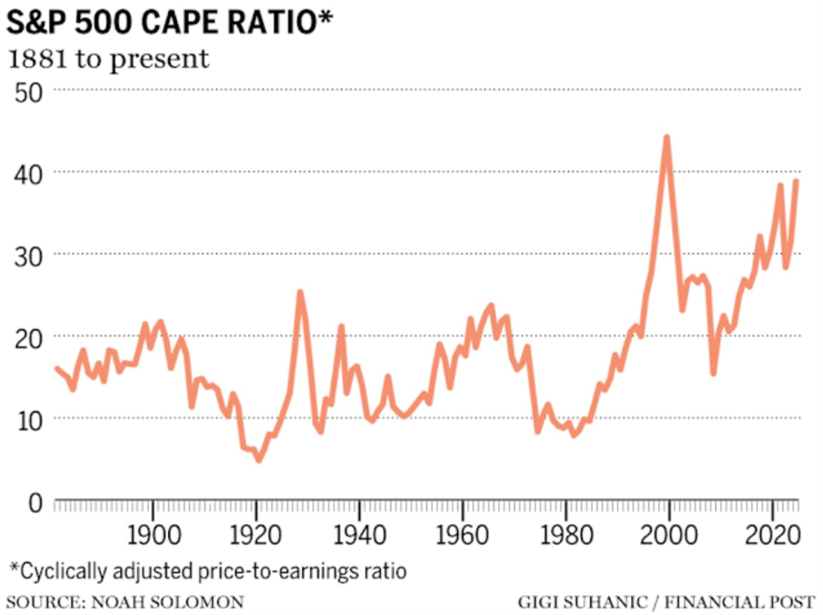

Case Shiller Cape Ratio

Although we have yet to reference the CAPE ratio in previous correspondence, it provides another way to illustrate market valuations, as compared to historical data. The CAPE ratio compares the current price of the S&P 500 index to the average inflation adjusted earnings over the past 10 years. As you can see below, the index is reaching levels it had only seen before the dot-com bubble burst, sending NASDAQ stocks down 80% over the next 2.5 years.

Now before we abandon all investment strategies and run for the hills, it is important to note that heated markets can last a very long time before they finally correct. The markets were considered to be overbought with an “irrational exuberance” coined by then Fed Chair Alan Greenspan in December 1996, over three years before the correction. It’s also relevant to share that this cycle is unique when compared to the dot-com era because many companies in the analysis are currently generating strong earnings that dwarf the ten-year averages used in the CAPE ratio. So, these charts are not predictors of what will inevitably happen, but instead useful tools in maintaining and motivating adherence to a prudent investment philosophy for preservation, income, and long-term sustainable growth.

Although it is a drum we have beating for a long time, as history has shown us, we still believe that diversification, quality, profitability, sound management, and reasonable valuations matter. We also want to avoid (and help our clients avoid) the temptation of stating the four most damaging words to a portfolio: “This Time It’s Different,” John Templeton.

Artificial Intelligence

We want to take a moment to speak into what has become one of the primary opportunities and primary concerns for investors over this past year. There is no question that artificial intelligence is a new dynamic norm that is transforming our world at levels almost beyond comprehension. We definitely believe it will continue to play a huge part in how we do just about everything moving forward. However, we have a concern as it pertains to the AI investing we are seeing, as does much of the broader investment community, which is why we have seen some recent tremors in the AI space. With trillions of dollars going toward AI it begs the question whether these companies can collectively produce earnings commensurate with all the dollars directed toward them. As with the dot-com craze of the 90’s and the subsequent tech bubble it created, is it possible that AI’s widespread competition, broad accessibility, and normalized utilization realities of the future will actually produce lower earnings and profitability than current pricing would support?

There seems to be a very real possibility that over the next few years, although it will be regularly utilized by almost everyone, it could be commoditized at a level where actual profitability and earnings from those AI engines, infrastructure, data centers, chips, and overall utilization will be far less than current investing may support over time. It seems to echo some of the same reasoning behind the hundreds of billions of dollars invested in the tech bubble in the late 90’s, justified by the fact that the Internet would change the world, which it has. However, the cumulative investments made at that time did not end up providing the hoped for returns and actually caused that 80% drop in the NASDAQ when that bubble burst from early 2000 to late 2002.

Accordingly, while we have maintained selective exposure to a number of AI related companies in our portfolios, we have been cautious with our exposure and will continue to avoid the temptation to overweight this segment. We continue to believe profitable companies with strong balance sheets and reasonable prices will not only provide strong growth moving forward but also position your portfolio for a more stable journey ahead if/when the markets incur a less favorable cycle of volatility.

Portfolio Review

As you can see, we have enclosed the update of your portfolio for review. While we are always pleased to see strong performance that moves your plan ahead of our original projections for growth, we are always frustrated when we underperform the blended benchmarks, which occurred in 2025. While our long-term numbers are still strong based on the relative allocations chosen with prudent diversification, our objective is always to achieve strong growth while still protecting against downturns when they occur. As outlined above, this unique cycle and our relative performance is somewhat a confirmation of the philosophy to which we adhere and an affirmation that we are following the prudent investing principles that are most likely to help you achieve your financial objectives as we look to the future.

Please take some time to review the enclosed report. Should you have any questions, concerns, or updates to your planning, please feel free to call. As always, we continue to consider it an honor and a privilege to work with you and your family and look forward to doing so for many years to come.

Kindest regards,

Michael Brocker

MSFS, CLU, ChFC, AEP®, AIF®

Chartered Financial Consultant

Masters of Science in Financial Services

Matthew Brocker

MSFS, AEP®, RICP®, CAP®, AIF®

Masters of Science in Financial Services

Josh Brocker

CFP®, AIF®