Dear Client,

We hope this update finds you and yours enjoying wonderful memories of summer, while at the same time welcoming in the autumn months and all the beauty they offer. Entering the fourth quarter we are riding strong market performance that has left the major market indices near their all-time highs which were reached last month. Equity markets have appeared to shake off the first quarter losses, which were driven primarily by tariff concerns. Not only have we seen a full recovery of those losses, but also strong performance numbers on most indices year to date as you’ll note on the performance summary attached.

Economy

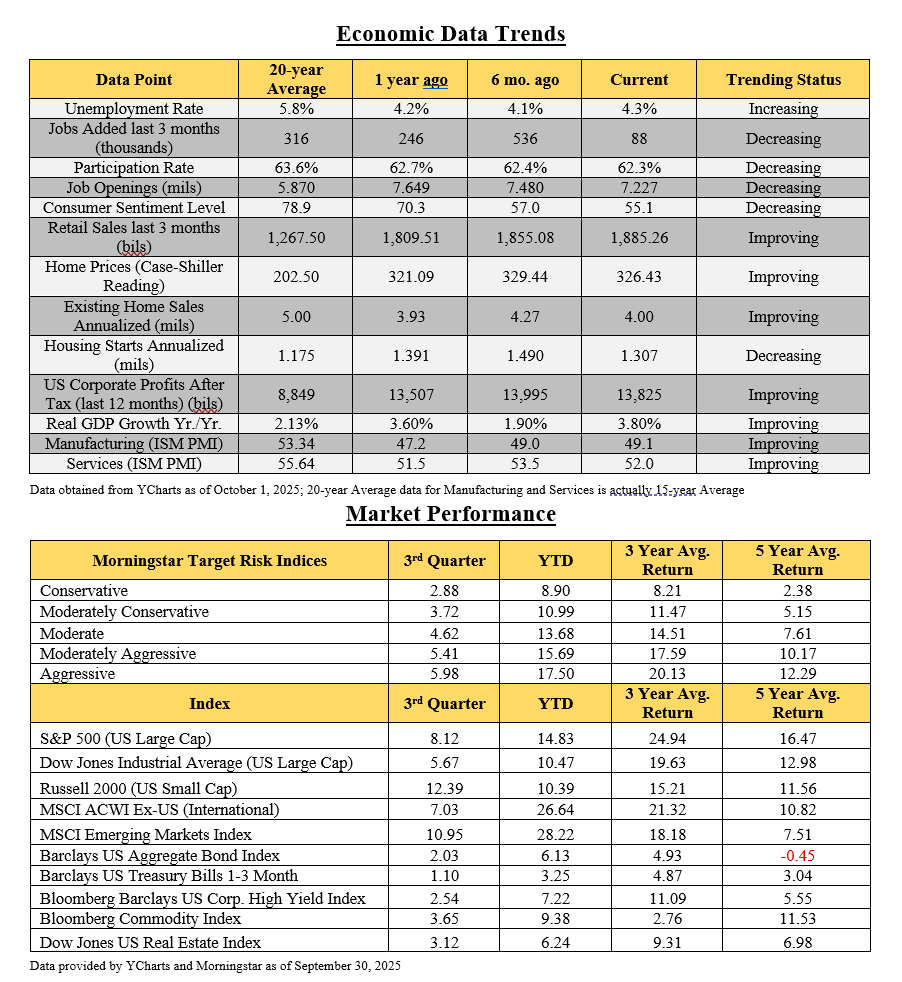

Although there is a strong push for economic growth from the current administration, there are indicators that leave room for more of a cautious optimism. On the plus side we have seen stronger than expected growth with GDP at 3.8% for the second quarter and estimates for the 3rd quarter revised upward to 3.9% or possibly 4%. Retail sales and consumer spending continue to be strong and have also exceeded forecasts. Unemployment is at 4.3%, which is still well below the 20-year average of just under 6%. And both housing and corporate profits continue to sustain relatively high levels compared with their long-term inflation adjusted levels.

However, there is much more to the story. Although growth has recently outpaced projections, it does appear to be slowing. Unemployment has also been ticking up gradually while job openings and participation rates are both decreasing, and we’ve also seen a significant reduction in jobs added over the last year. Inflation also appears to be on the rise and is still above the Fed’s 2% target, now closer to 3%.

The Fed has started to move to a more accommodative stance, and the market is projecting two more rate reductions prior to year end. While this should be good for economic growth there is significant debate surrounding the newly established tariffs and their impact on projected economic expansion. Many economists believe income generated by the tariffs will help to offset the new tax cuts, which makes sense. However, the bigger concern is whether or not the tariffs could create higher inflation and whether or not a more accommodative Fed and/or more robust economic growth will be enough to keep the economy on strong footing. While we hope for robust growth moving forward, we are definitely sensitive to the fragility of the economy and the impact it can have on the markets moving forward.

Markets

As mentioned above, the markets recently surpassed their all-time highs and have provided nice (albeit a bit bouncy) growth over the past several years. However, as mentioned in previous updates, valuations are feeling a bit stretched. At the risk of getting a bit technical, the 30-year average PE (Price to Earnings) ratio for the S&P 500 is just under 17, and currently it is approaching 23. This represents a 40% overvaluation and what’s even more concerning is that the largest 8 companies now represent close to 40% of the weight of the index, and their average PE is over 35. While these 8 companies have continued to perform well again this year, and may continue to over the years ahead, they have collectively pushed valuations to exceedingly frothy levels that provide some concern.

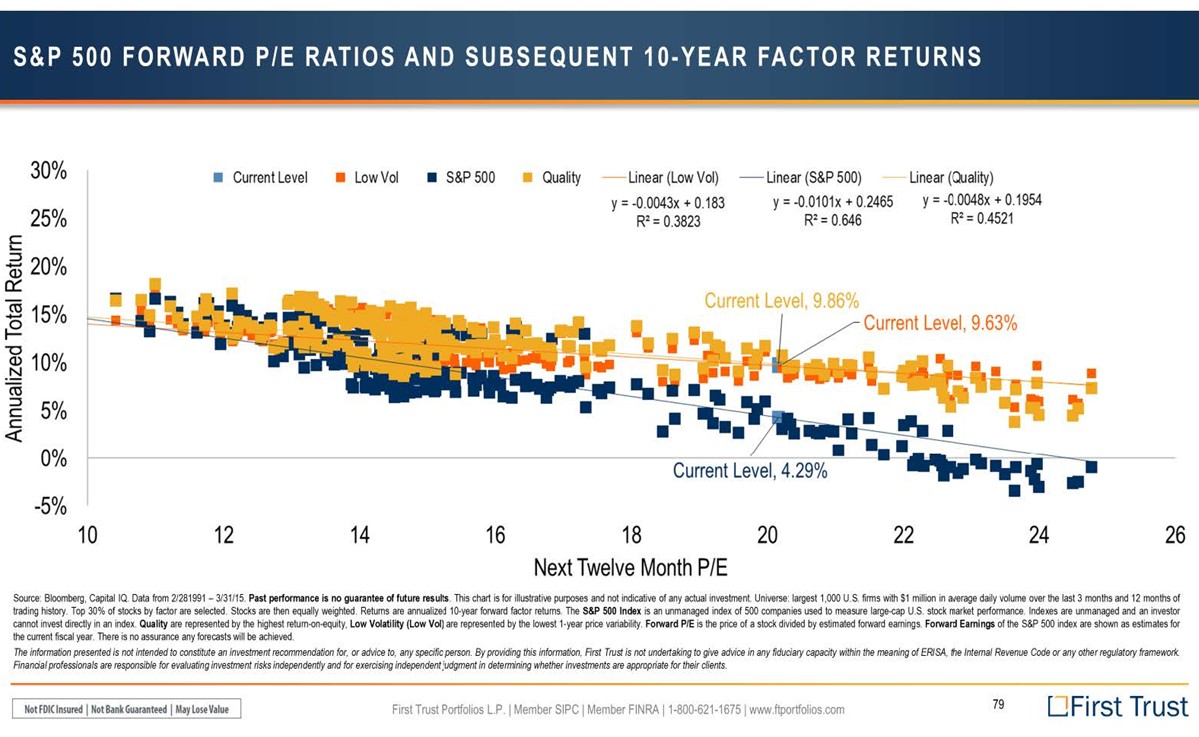

We apologize for all the detail on the following scatter chart, but we wanted to illustrate what the markets have seen historically when valuations are pushed to extreme levels and help to illustrate why we believe that now more than ever, high quality and reasonable valuations matter. Not only to protect if we see a slowdown in the economy, but also to provide what we believe will be stronger growth potential as we look out over the next 5-10 years. The “X” axis shows PE Ratios, and the “Y” axis shows the annual average return per year over the subsequent ten years. The dot plots are showing each ten-year period recorded.

As you can see the data is pretty compelling, as it reflects that higher quality companies as defined have historically performed much better than lower quality when PE’s get higher. You’ll also note that the chasm between the two widens the farther you go out to the right. Although past performance is not a guarantee of future performance, this helps us affirm our philosophy of maintaining broad diversification of quality companies across a wide spectrum of styles, sectors, and regions to obtain not only lower volatility, but what we believe will be stronger growth as well.

Portfolio

Please take some time to review your enclosed performance update. As you will note we continue to see solid growth this year along with the broader markets. Although we are concerned when our portfolios are lagging behind their blended benchmarks in any year, this year we are not surprised. It actually affirms the quality and valuation metrics that we apply to your holdings in an environment of what many analysts would regard as irrational exuberance. As we look back to the bear market just a couple years ago, we were able to preserve on the downside vs. the indexes whereby our 5-year numbers still look very strong vs. the blended benchmarks. More importantly, as illustrated above, we think your portfolio is well positioned for achieving your financial objectives and navigating the currents ahead.

Before signing off we have an exciting announcement to share that my daughter, Beth, has recently joined the firm. Beth graduated from Bethel in 2024 majoring in finance and gained additional experience working much of the last year at Ecolab in their finance area. She will be focusing her efforts primarily with our planning and advisory team as we look ahead. We are very excited for her joining the firm and the start of her career with Legacy.

Please take some time to review the enclosed update and if anything has changed regarding your planning objectives, financial situation, or anything else please give us a call. If we have not heard from you, we will be in touch as we near year end as appropriate. As always, we consider it an honor and privilege to work with you on your planning and portfolio management and hope to do so for many years to come.

Kindest regards,

Michael Brocker

MSFS, CLU, ChFC, AEP®, AIF®

Chartered Financial Consultant

Masters of Science in Financial Services

Matthew Brocker

MSFS, AEP®, RICP®, CAP®, AIF®

Masters of Science in Financial Services

Josh Brocker

CFP®, AIF®