Dear Client,

Hoping you and yours enjoyed a wonderful Christmas and great excitement for the New Year. Although the previous year brought many challenges which included ongoing conflicts overseas and a vitriolic election cycle at home, there is a sense that things may be moving in a better direction for 2025.

Over the last year, Israel has effectively diminished the military threat from Hamas and Hezbollah, and with the fall of the Assad regime they have now been effectively dismantling the weaponry left behind in Syria to reduce the likelihood of terrorist factions possibly using these weapons against them. It also seems there is a high motivation to bring the Russia/Ukraine conflict to an end from the new administration, which would certainly be welcomed considering the hundreds of thousands who have died on both sides. Although political parties have always been and will always be contentious by nature, it appears the nation is more aligned than it has been in recent years. It’s been encouraging to see some forces that have been diametrically opposed, now making efforts to work together for the greater good of our citizens.

The Economy

While it’s difficult to really know whether the economy is good or bad while going through an election cycle, the reality is that the economy is doing relatively well, but far from perfect.

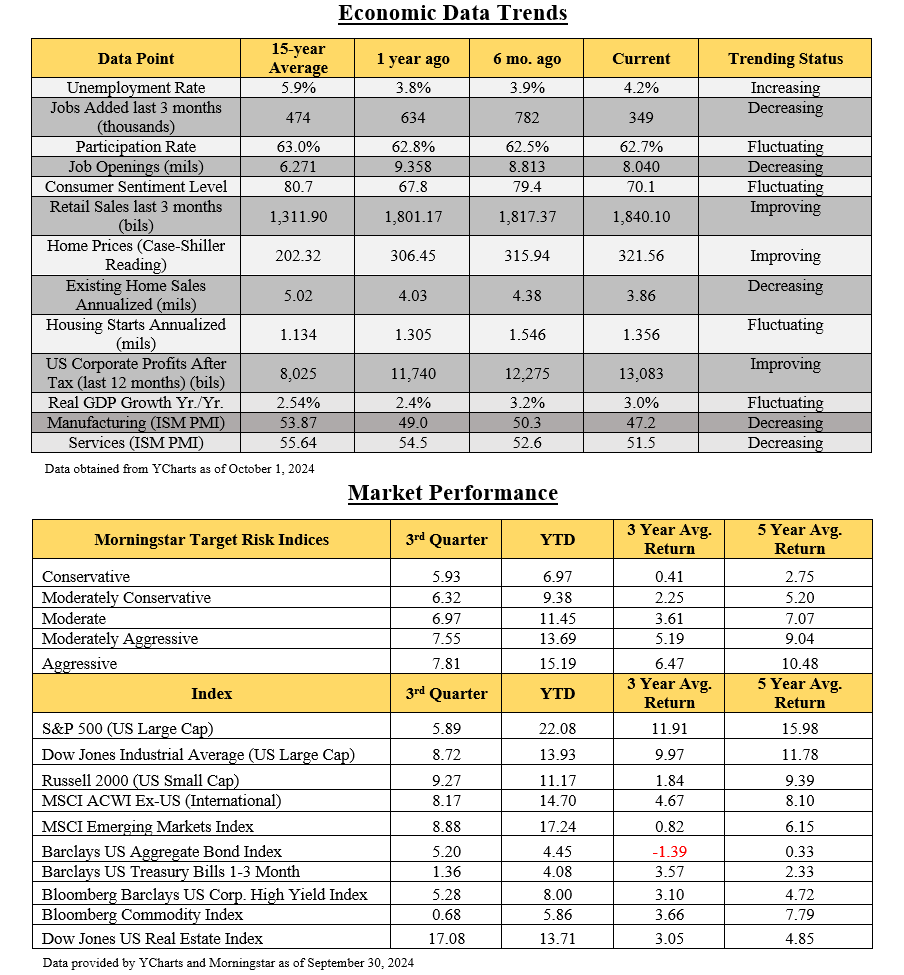

For example, on the employment front, it has been encouraging to see unemployment maintained just above 4%. However, it’s been of concern that “jobs added” data was somehow overstated by more than 800k during the year, that many of those jobs were provided by the government, and that the Job Opportunities Index has dropped by over 30%.

It’s also been encouraging to see home values continue to increase and new housing starts maintained at historically high levels. However, it is disconcerting that the affordability crisis and high mortgage rates are making the purchase of a home less affordable for first time homebuyers, which will potentially have a negative impact on the housing market as we look ahead.

It’s also been encouraging to see Retail Sales, Corporate profits, and GDP continue at levels well above their 15-year averages. However, there remains a question as to whether these indicators may have been propped up a bit with the 5 trillion dollars of stimulus (money printing) that occurred a couple of years ago and the corresponding inflation that ensued. Along with the stimulus checks, citizens have been debt financing their standard of living more than ever before, with consumer debt levels currently sitting at record levels, which is an obvious concern.

New Administration

As we look ahead, a number of the administration’s new initiatives should bode well for the economy if stated objectives are met. Lowering corporate taxes, extending the Trump tax cuts, reducing excessive regulations, incentivizing companies and other countries to invest in the US, and other growth strategies will hopefully strengthen the economy. The administration’s concerted effort to lower energy prices by as much as 50% over the next year through drilling, fracking, and reopening pipelines should help create greater energy efficiencies, also helping to keep inflation below 2%. Lower energy prices not only benefit consumers directly, but also companies that rely on energy to manufacture their products or provide their services.

The new administration’s strategies surrounding tariffs and their potential negative and/or positive impact have become a primary concern. The fear is that these tariffs will create higher prices for the consumer (aka inflation). However, while tariffs may or may not increase prices on select goods, it is important to realize that businesses and consumers are both pretty savvy when it comes to accessing products in the most cost-efficient way. For example, while one country may not be able to offer their goods at as competitive a price as previously due to “potential” tariffs, other countries and/or companies may now fill that void with more cost competitive solutions. So, a reduction in imports from one country paying higher tariffs may beget an increase in imports from another country that is paying lower tariffs. Also, not to be missed is the fact that our president elect is a master at the “Art of the Deal,” whereby many feel that the threat of exorbitant tariffs to some countries are really just negotiating tools to encourage them to embrace a more favorable trade stance for the US, and/or to leverage the tariffs to motivate other countries to follow the administration’s recommendation’s in other areas, like border security.

US Equity Markets

While the markets, as measured by most indices, had significant increases over the year, the new initiatives set forth by the upcoming administration will likely beget increased uncertainty and associated volatility within the markets. A simple example occurred when the market rallied nicely for several weeks after the election (with maybe a hint of irrational exuberance), and then proceeded to give back much of those gains over a consecutive 10 day stretch of declines before Christmas, the longest stretch in 50 years. Keep in mind that as each policy initiative plays out and the Fed intercedes with their monthly outlooks, in most cases fluctuations move things in more favorable directions, which is obviously the hope for the years to come.

Although historically small caps and mid caps have outperformed larger companies, US large caps continued their encouraging pace last year. As you can see in the attached performance report, the larger companies as measured by the S&P 500, have definitely been the biggest drivers of growth in recent years. Part of the fuel for this dominance of the large caps can be credited to the largest 7 companies of the S&P 500, which now represent over one third of the total market cap of the S&P 500. While these returns have been encouraging, the valuations of these mega caps continue to be a concern.

These 7 companies combined for an average return of approximately 50% in 2024, however they also share an average price earnings (PE) ratio of approximately 50 as well. The other 493 companies have PE’s closer to 17 or 18. In other words these 7 largest companies (1/3rd of the S&P 500 weighting) are trading at 50 times their earnings and are arguably significantly overpriced. We maintain very limited exposure to these companies, understanding regression to the mean can, and historically has occurred when companies reach these stretched valuations. The risk is that these holdings may either experience lower price momentum than the broader market moving forward or experience stronger downside exposure when an inevitable market correction occurs. We do, however, have a much higher comfort level with many other quality companies within your Legacy Portfolio whose valuations are more in line with reasonable PE’s. This should not only give more room for growth at a reasonable price, but also stronger protection against downside risk during adverse market cycles.

International Holdings

Although non-US holdings have lagged behind the US markets for several years, international valuations are currently very favorable. Here again, we believe long-term growth opportunities still exist in several global markets and that having global diversification will not only help reduce volatility within your portfolio, but also help mitigate the currency risk that seems prevalent with the ever-increasing strength of the dollar. Our strategy to embrace excellent companies based on our evaluation of preferred holdings from eleven premier international money managers, has provided solid results that continue to outperform the MSCI ex-US index since inception. We maintain good diversification within various sectors with companies positioned for solid growth potential looking ahead.

Interest rates and Fixed Income Markets

While the Federal Reserve’s approach to interest rates in 2025 remains a bit of a mystery at this point, the likelihood of an increase in rates seems very remote. Based on comments made and analysis we have thus far, we believe 2-3 rate cuts could occur in 2025. Much of this will play out in accordance with how things progress with the economy as well as the Fed’s interpretation of the leading economic indicators. Not to be missed is the likelihood that the Fed Chairman may also be receiving some “mild” pressure to bring down rates in an effort to fuel stronger economic growth.

While bond holdings had been yielding roughly 2-3% in diversified portfolios prior to the Fed’s dramatic increase in rates, we are now seeing our diversified fixed income holdings yielding between 5%-6%. This has been a welcome sign and has helped to remove the “penalty” of diversification through better yields. Our bond managers continue to purchase investment grade bonds with short to intermediate term maturities, which we believe to be prudent amid the continued uncertainty surrounding interest rates and the fixed income markets.

Alternatives

Alternatives came onto the scene as an important allocation within a properly diversified portfolio in only the last couple of decades and strong performance recently has helped enhance overall returns. Alternatives that we hold within your portfolio include precious metals, commodities, real estate, and digital currency. The objective of these holdings is to not only reduce the correlation with stocks and bonds, but also to enhance growth over time. We initially held a smaller allocation closer to 5% on average, and over the last couple of years moved closer to a 10% allocation to help reduce the correlation coefficient even further, seeking stronger long-term performance as well. Your actual allocations to the alternatives sleeve are within your report for review.

Portfolio

As you’ll note, we’ve experienced another encouraging year of solid performance and strong recovery from the most recent bear markets of 2020 and 2022. We’ve been pleased to see your net performance numbers continue to be very strong in comparison to the appropriate Morningstar Target Risk Benchmarks. Possibly of even greater importance, we have a high comfort level with the overall asset allocation as we look forward, maintaining a cautiously optimistic view of the year ahead. We continue to implement proactive portfolio rebalancing as appropriate, with high sensitivity to the associated tax impact. Although tax loss harvesting opportunities were minimal in 2024, we continue to implement them as the opportunity avails.

Please take some time to review the enclosed updates and should you have any questions or concerns, please reach out at any time. Also, if you have significant changes to your planning objectives or financial circumstances, let us know and we will connect to review appropriate updates to your strategy. As always, we consider it an honor and a privilege to serve you, and look forward to helping with you planning and portfolio management for many years to come.

Kindest regards,

Michael Brocker

MSFS, CLU, ChFC, AEP®, AIF®

Chartered Financial Consultant

Masters of Science in Financial Services

Matthew Brocker

MSFS, AEP®, RICP®, CAP®, AIF®

Masters of Science in Financial Services

Josh Brocker

CFP®, AIF®