Dear Client,

We hope this update finds you enjoying another beautiful fall season and quality time with family and friends as the holiday season is just around the corner. With the election looming and changes in the White House on the horizon, we have provided some analysis we believe may be helpful as we look to the end of the year.

Markets

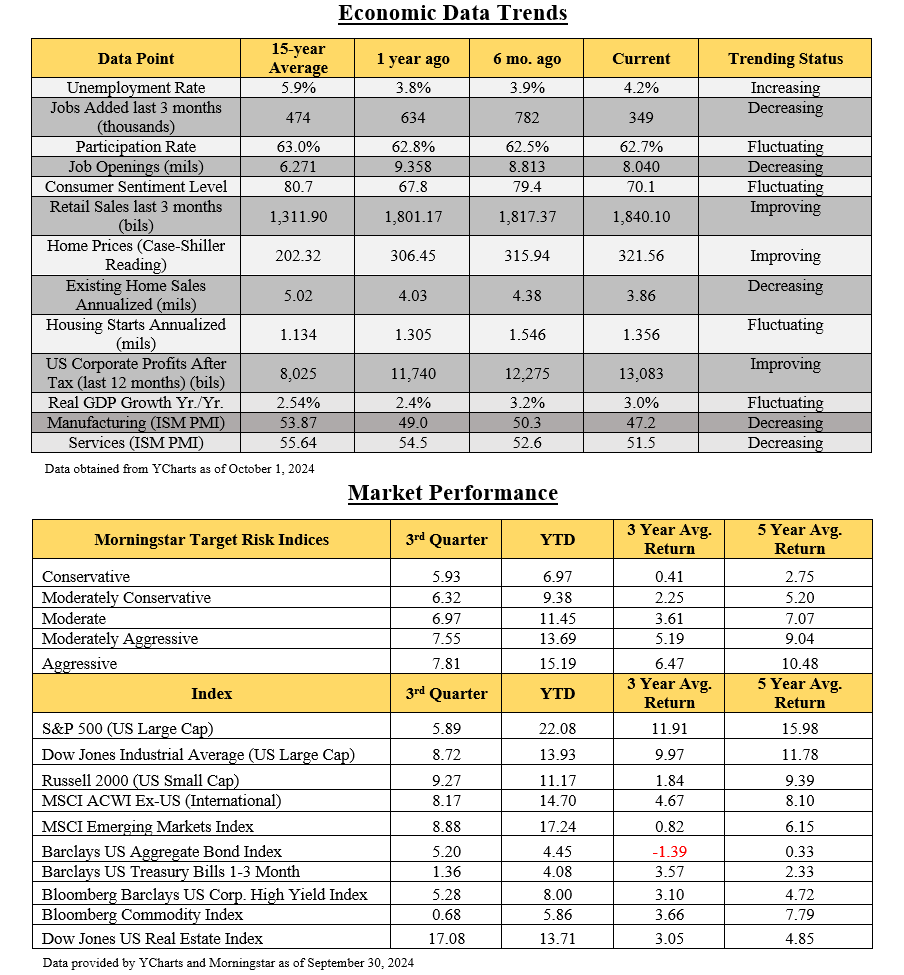

The equity markets have continued to grind higher through soft patches in performance and much uncertainty about what the future may hold. Several indices have reached all-time highs as investor confidence has remained relatively strong and valuations of some of the largest companies push well above historical averages. For the year, most of the major equity indexes are reporting double digit gains, meanwhile bonds have experienced more mild results in line with longer term averages. More detailed performance including balanced benchmarks are attached for your review as well.

Economy

The Federal Reserve finally started their long-awaited monetary easing, lowering rates 0.50% a couple weeks ago, with the intention to continue rate cuts over the months ahead. The .50% reduction was more than some were expecting and could indicate that the Federal Reserve believes the economy isn’t as healthy as initially thought. However, it was received well by the markets overall as the S&P 500 went up 2.3% from the day of the announcement to the end of the quarter. The Fed Chair Jerome Powell has made it clear that The Fed does not want to make the mistake of cutting rates too aggressively with uncertainty regarding inflation still looming as a primary concern. On the flip side, some fear the Fed has waited too long to lower rates whereby the soft landing we all hope for may turn out to be a bit rougher. With manufacturing slowing, consumer savings balances diminishing, and credit card balances reaching all-time highs, the question is whether or not there is enough fuel in the economy to sustain the earnings growth the market seems to be expecting. While these items hang in the balance, a prudent approach of quality holdings and proper diversification remains a very high priority.

Election

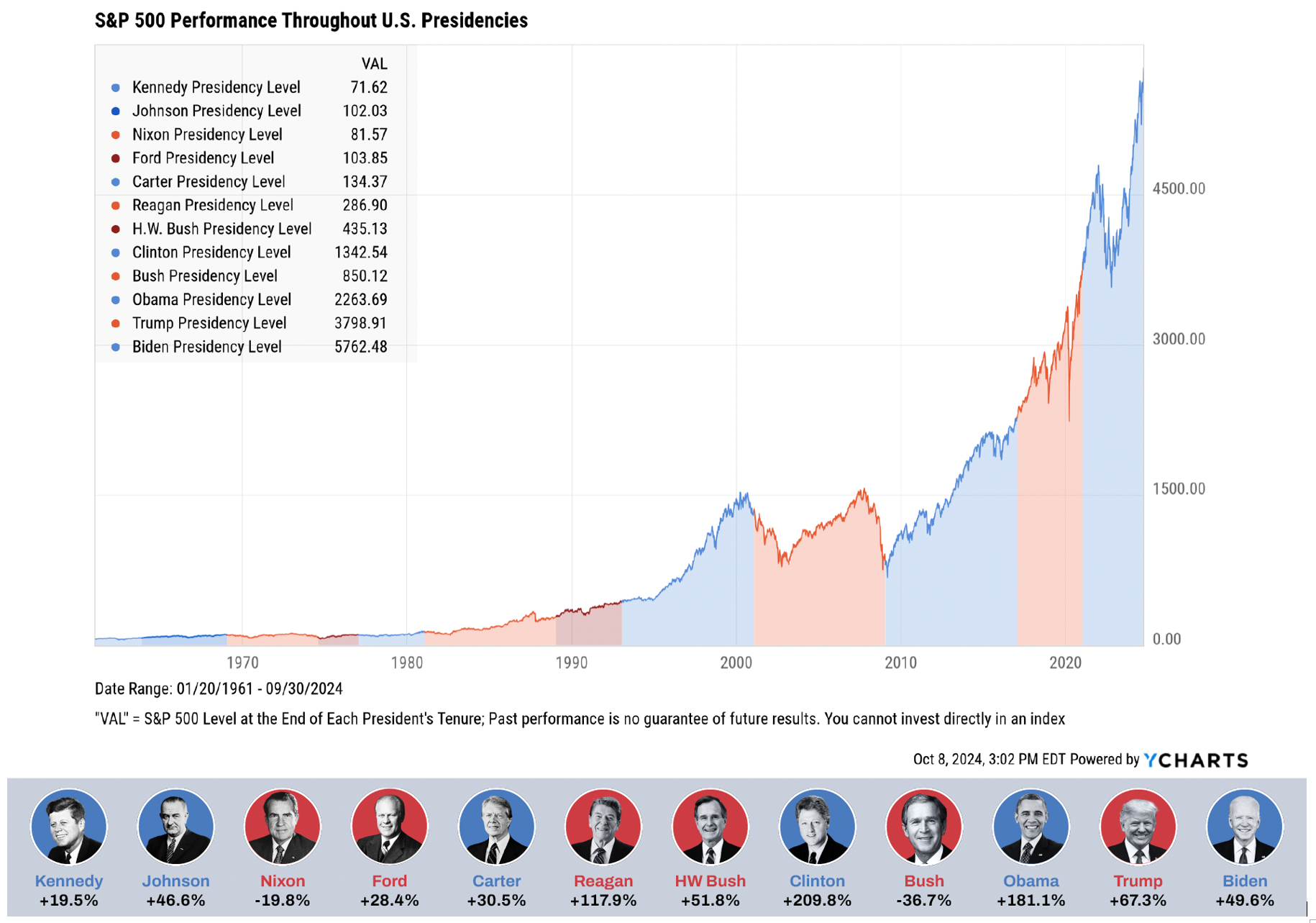

With just over a month until the Presidential Election, many people are concerned with not only the outcome of the election, but even more so, the perceived impact. Over the years, it seems there are always willing pundits who interject a profound certainty pertaining to inevitable catastrophic outcomes if one candidate were elected vs. the other. These concerns have played out over the last several elections, and once again seem to carry a narrative that we are doomed to either have an autocratic dictator, or a liberal Marxist. While you likely have an affinity toward one candidate or the other, history has proven that both the economy and the markets are driven by much more than who happens to sit in the White House.

It is important to note that the economy and the markets have a natural ebb and flow that can and will occur regardless of who is in the White House. The market is also subject to systemic risk factors as well. For example, in the 2008 Financial Crisis both President Bush and Obama participated in the 57% decline of the S&P 500 over an 18-month drawdown. The Global Pandemic of 2020 also brought a 34% decline in the market and a negative ripple effect on the economy that was for the most part out of the control of Presidents Trump and Biden. Although we believe it is clear that policies relating to taxation, regulation, and geopolitics have an impact on the economic health of our country, see the correlation to the party in the White House is less significant than most perceive.

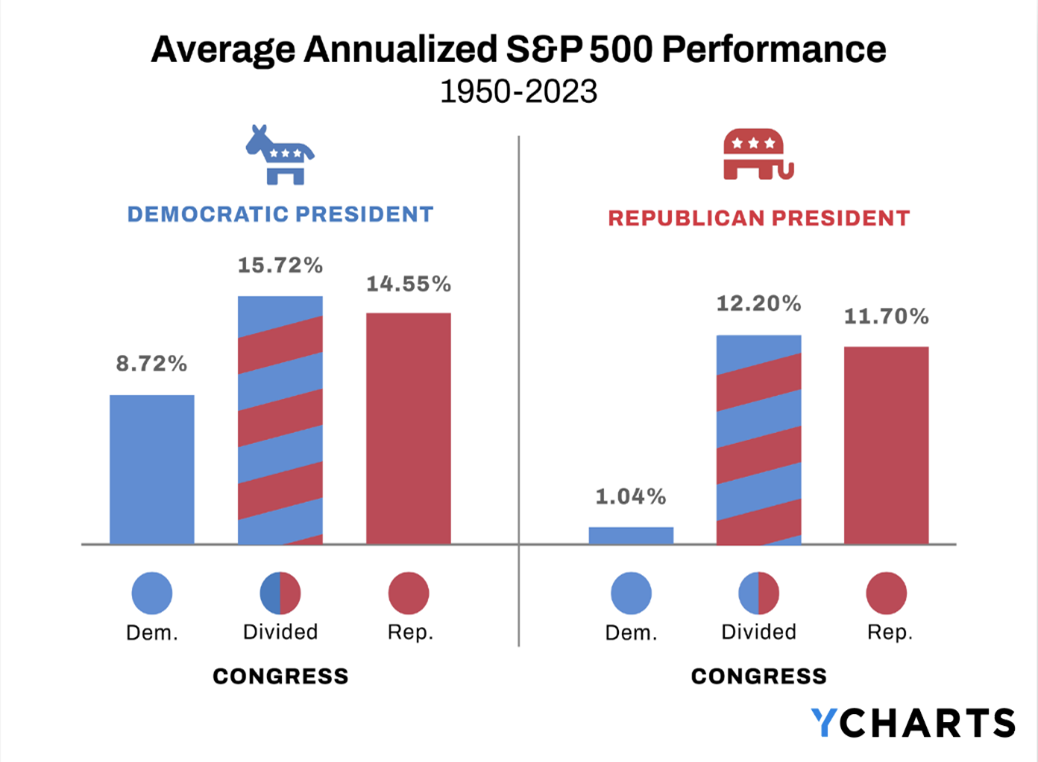

Another interesting analysis shows that over the last 73 years, a balanced Congress has actually provided the strongest average returns. Additionally, market performance has historically been stronger with a Democrat in the White House, although the Republican platform is considered to be more pro-growth with lower taxes and deregulation. The main takeaway for us is that regardless of who is in the White House, owning companies (stocks) seems to be a prudent component in proper asset allocation when seeking to optimize long term growth in a manner consistent with your time frame, risk propensity, and overall financial objectives. While elections always seem to bring short-term volatility and uncertainty, focusing on longer-term objectives should always be the most important component in portfolio management.

Portfolio Update

Your most recent quarter end report is enclosed for your review. We have been pleased to see that both your short-term and long-term net performance has been very strong vs. the appropriate blended benchmark and at this point we are not recommending any allocation changes. We continue to conduct rebalancing as the opportunity avails, along with embracing tax loss harvesting as we are able. As you review your updated report, please feel free to call with any questions or concerns you may have. If we have not heard from you, we will continue to keep in touch as appropriate.

As always, we consider it an honor and privilege to be working alongside you with your planning and look forward to doing so for many years to come.

Kindest regards,

Michael Brocker

MSFS, CLU, ChFC, AEP®, AIF®

Chartered Financial Consultant

Masters of Science in Financial Services

Matthew Brocker

MSFS, AEP®, RICP®, CAP®, AIF®

Masters of Science in Financial Services

Josh Brocker

CFP®, AIF®