Dear Client,

We hope this letter finds you and yours enjoying the beautiful summer months and all the blessings this time of year has to offer. Amid July 4th celebrations, we also gratefully reflect on our independence and the freedoms we enjoy in our imperfect, yet wonderful country. As we reach the midpoint of the year with an economy that seems to be softening and yet markets that have continued grinding higher, the real question seems to be “What does this mean for me, and should we be doing something different?” We have some insights and recommendations to share that we hope to be helpful as we navigate a perpetually uncertain future.

Economic Insights

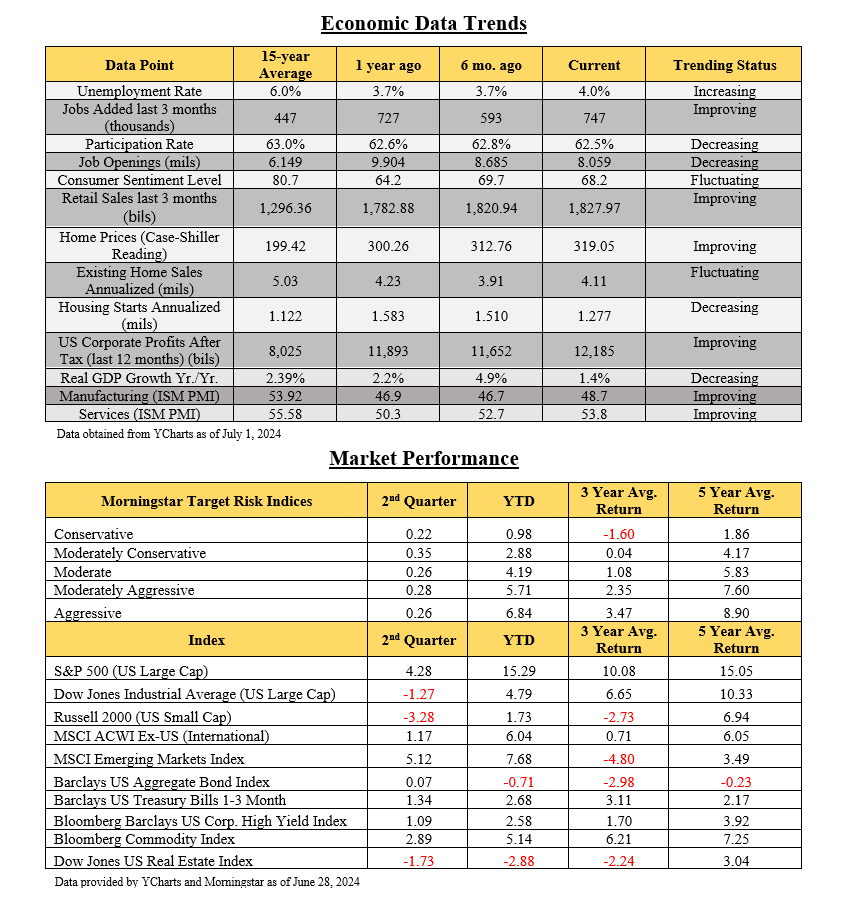

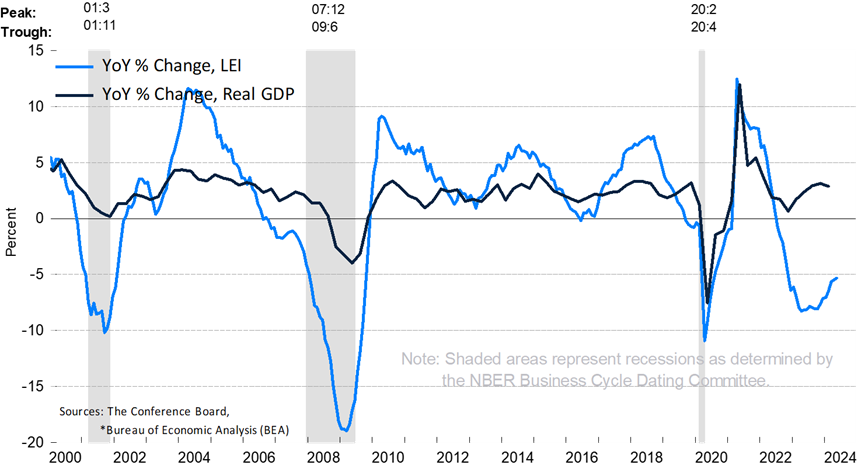

As you’ll note in the enclosed update, we are definitely seeing signs of a slowing economy. Both services and manufacturing sectors are treading water, while housing and automotive are also showing signs of slowing. The University of Michigan Consumer Sentiment Index fell from 79 in March to 65 earlier in June. Amid all this, consumer spending remains strong in what appears to be an inexplicably resilient economy. Consumer spending is helping to keep retail sales and corporate profits at historically healthy levels. This, along with recent growth in real wages, is causing many economists to believe any chances of recession may be further down the road, if at all.While the Leading Economic Indicators (LEI) index is still at historically low levels, it is showing recent signs of improvement. This, coupled with other bright spots on the economic front like lowering inflation, growth in real wages, and low unemployment, allow us to approach the horizon with cautious optimism.

As referenced in earlier updates, much of the fuel for growth and consumer spending came from trillions of dollars of stimulus infused into the economy which increased excess savings, of which have now mostly dissipated with ongoing spending. In addition, savings rates have been more than cut in half, and many consumers are debt financing their consumption with credit cards, whereby balances and defaults have increased significantly over the last 1-2 years. Also worthy of note is the fact that much of the job growth we are seeing is in government created jobs, which may not be a true indicator of actual employment health.

All this to say, while we are more optimistic by nature and always hope for the best, we think it is prudent to be prepared for a potential slowing of the economy and possibly even a recessionary period in the next 12-24 months. It is obviously very difficult to get a handle on the future direction of the economy, but we believe it is particularly challenging with all the variables currently at play, and even more so during an election year. During an election year, it is difficult to decipher where things are really at with the economy. It is also important to note that depending on Fed actions, geopolitical forces and election outcomes with subsequent policies enacted, outlooks can and do change.

Market Observations

The markets have continued to move forward pressing up against all-time highs, which seems to be driven by positive investor sentiment as much as anything else. There seems to be a belief that the growth outlook continues to be very positive and if we begin to see signs of weakness the Fed will lower rates to help maintain these higher market levels and encourage growth. This “goldilocks” scenario may in fact play out as hoped, but we believe there are pockets of the broader market that are grossly overvalued whereby active management is critical to properly navigate what we believe to be an uncertain and potentially volatile cycle on the horizon.

An example of overvaluation is reflected in the 10 largest stocks of the S&P 500. Their current price is approximately 30 times their forward earnings, which is almost 50% above their average PE for over 25 years. At the same time, the rest of the 490 stocks in the index are trading at an average of only 17.5 times their forward earnings. Sensitivity to valuations is especially important when market fluctuations may be on the horizon, but historically when segments of the market are significantly overvalued a regression to the mean occurs, whereby more favorably valued segments of the markets provide better protection against downside exposure and better opportunities for growth.

Portfolio Updates

While we are definitely maintaining a strong position in US large cap companies, we continue to be very selective and based on the aforementioned. We also believe that now it is as important as ever for you to maintain a prudent broadly diversified approach. Valuations in mid caps, small caps and international stocks have more favorable prices in relation to their earnings when compared historically. In fact, non-US developed markets have a forward PE of only 14.2, which we believe creates some great value opportunities and should help to mitigate currency and market downside risk as well.

As you will note on your updated report, overall performance has been strong, and we are thankful to see your net performance numbers versus the blended benchmarks showing very favorably. Our managers have continued to maintain solid results vs. their relative indexes, and your alternative holdings have also provided some additional growth beyond a traditional stock/bond portfolio. We continue to implement strategic rebalancing, tax loss harvesting, and screening as appropriate on the Legacy Portfolios, and at this time we are not enacting any other significant changes to your overall strategy.

Please take some time to review your customized report and should you have any questions or concerns, or if your objectives have changed in any way, please let us know. As always, we consider it an honor and a privilege to work alongside you with your wealth management, and we look forward to helping you with your planning and portfolio management for many years to come.

Kindest regards,

Michael Brocker

MSFS, CLU, ChFC, AEP®, AIF®

Chartered Financial Consultant

Masters of Science in Financial Services

Matthew Brocker

MSFS, AEP®, RICP®, CAP®, AIF®

Masters of Science in Financial Services

Josh Brocker

CFP®, AIF®