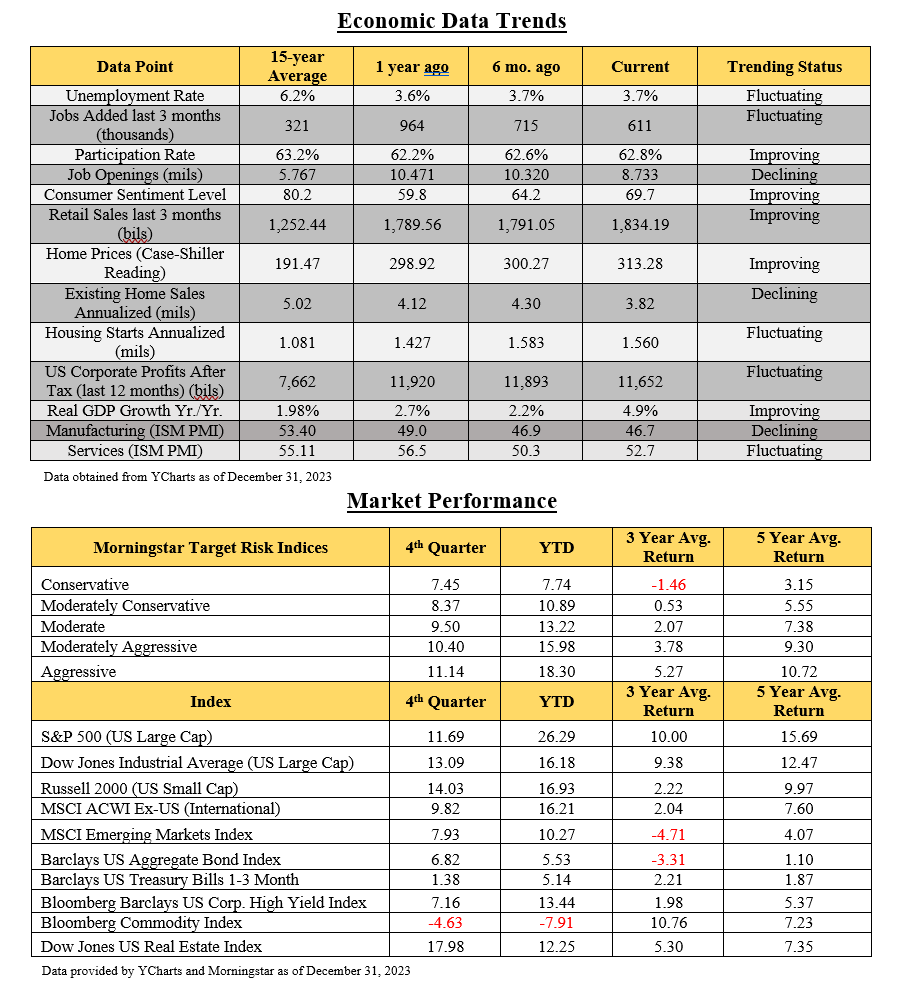

Dear Client,

We hope you and your family are doing well as we reflect on 2023 and look forward to the year ahead with great expectations. Having experienced a year in which many around the globe suffered through the pain of war, famine, loss of loved ones, and natural disasters, we are thankful to work with so many of you who prioritize helping others in need through the support of ministries both at home and abroad. Although 2023 was a year of turmoil, it was also a year in which the markets provided some needed recovery from a lackluster 2022. For the year, most equity/stock indices posted double digit returns, while alternatives in the managed portfolios provided even more impressive results. Bond holdings also posted positive results this year, following historically poor results from the previous year due to the rising interest rate environment.

The Markets

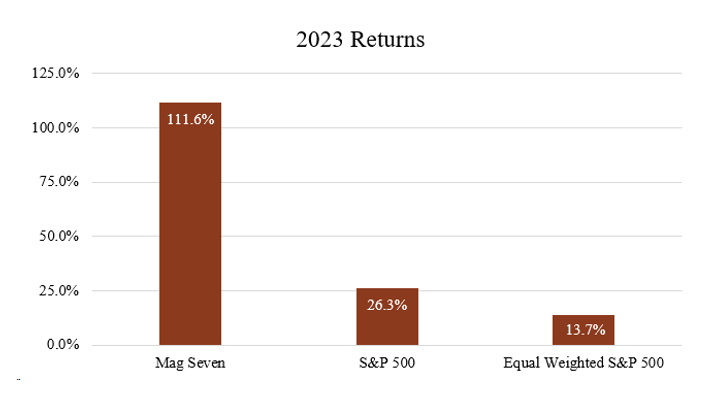

As touched on in previous updates, this year’s growth on the US large cap index (S&P 500) was generated in a very nontraditional fashion, with just 7 stocks (“Mag Seven”) of 500 accounting for most of the return for the index which was up over 26% for the year. The average return of these seven stocks was 111.6% and currently they represent 33% of the S&P 500 index as it pertains to return. The equal weighted S&P 500 return was only 13.7%, which included these stocks. Accordingly, we have seen the greatest disparity in returns between the equal weighted S&P 500 vs. the market cap weighted index since 1998.

As we look forward one might ask if it makes sense to have a heavier weighting to the very largest stocks, but looking back over the last 52 years through the end of 2022 we have found that the equally weighted returns of the S&P 500 has actually provided stronger growth than the cap weighted by 1.7%/year, not to mention that broader diversification historically provides for lower volatility as well.

Another question that comes up frequently when the Dow is reaching all-time highs is whether or not the market is overpriced and due for a correction. As we look at the S&P 500 an argument could be made that it is slightly overpriced when looking at the PE Ratio for the index as a whole. What is interesting is that when you look under the hood, the stocks that are arguably the most overvalued today are that same Mag Seven that provided most of the growth last year with an average PE of 50. Whereby, the PE of the entire S&P 500 is currently at 19.51, leaving the understanding that the 493 companies that don’t represent the Mag Seven have an even lower PE than the long-term historical averages of the S&P 500. Looking forward, based on both historical data and current information, we believe that maintaining broad diversification will not only help mitigate potential downside risk, but also enhance long term growth as well.

The Economy

At the most recent meeting of the Federal Reserve, Jay Powell seemed to tip his hand regarding ongoing rate hikes in the near term and may even begin to lower interest rates 2-3 times or as needed next year. This has provided optimism in the stock market, boosting the Dow to all-time highs and providing a somewhat optimistic outlook for 2024. After raising interest rates 5.25% over an 18-month period, our greatest concern is the potential lagging impact this could have on the economy, believing the full effects may be yet to come. However, many economists believe that if we see a lag effect, the Fed is now equipped with the ability and willingness to lower rates to help provide a soft landing to a slowing economy, and thereby help sustain ongoing economic growth.

The most recent update on consumer prices showed a 2.6% increase over the last 12 months, which is moving very close to the Fed’s targeted 2% inflation rate, whereby ongoing rate increases are highly unlikely. Going back over the last 6 rate hiking cycles, the market has historically performed well over the 12 months following a final increase, averaging 17.6% according to analysis done by JP Morgan, going back to 1984.

Another point of interest is that we have just entered into another Presidential election year, which historically bodes well for the market, providing positive returns 83% of the time. While this could be due to a number of factors, you can rest assured that the powers that be will be doing everything they can to provide a strong economy and solid market performance, prior to the election in November.

Finally, you will note on the enclosed economic update that there are a number of indicators that are trending in a less favorable direction, which frankly was to be expected when the Fed started raising interest rates so aggressively to stave off inflation. However, we also take into consideration that many of those factors, like unemployment, remain favorable when compared to longer term averages, and are currently in reasonable ranges for sustainable growth. This holds true especially when taking the other aforementioned factors into consideration regarding the Fed’s ability to lower interest rates along with political motivations to induce economic growth and strong market performance this year.

Political/Geopolitical Realities

While a case statement can be made for ongoing economic and market growth in 2024, we remain concerned about the political and geopolitical forces that may impact U.S. and World economies. These include: The war between Israel and Hamas; War in Ukraine; U.S. involvement in said wars; Multiple litigations against our past president; Impeachment inquiries pertaining to our current president; Congress’s inability to gain alignment on a host of things ranging from the budget, to the border, to support for Ukraine and Israel. All these factors give us pause and will make for an eventful year, but none of them cause us to move from our best recommendation to optimize your financial outcomes in a manner consistent with your planning objectives. Maintaining broad diversification within a professionally managed portfolio that is allocated in a manner consistent with your objectives for asset protection, income and long-term growth remains our most prudent strategy as we look ahead.

Portfolio Update/Review

As you can see, we have enclosed the most recent update of your holdings through Legacy Wealth, which is also accessible through our free Legacy Wealth App if you prefer the electronic version. We are pleased to see your managers continuing to post solid returns when compared to their appropriate benchmarks, which is helping to fuel strong net performance when compared to the Morningstar Target Risk Indices enclosed. We continued to strategically rebalance as needed to maintain proper allocations within your managed portfolio, continually buying low and selling high to further optimize returns. We also conducted several rounds of strategic tax loss harvesting last year to help mitigate taxes whenever available and appropriate. Finally, we continue to monitor the companies maintained within your portfolio to avoid companies generating profit from activities inconsistent with your values.

Please take some time to review the enclosed update and should you have any questions or concerns, or if your objectives have changed in any way, please feel free to call. As always, we consider it an honor and a privilege to be working with you to help manage your finances and look forward to doing so for many years to come.

Kindest regards,

Michael Brocker

MSFS, CLU, ChFC, AEP®, AIF®

Chartered Financial Consultant

Masters of Science in Financial Services

Matthew Brocker

MSFS, AEP®, RICP®, CAP®, AIF®

Masters of Science in Financial Services

Josh Brocker

CFP®, AIF®