Dear Client,

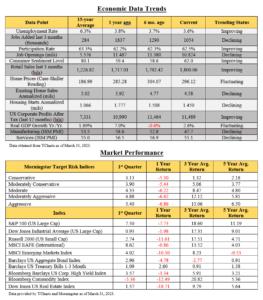

We hope this update finds you and your family flourishing as we enter springtime in anticipation of warmer months ahead. The first quarter continued a recent pattern of market volatility, economic uncertainty, and geopolitical tensions that now almost seem to be the norm. Although we’ve seen bumpy markets since the first of the year, we were encouraged to see most major indexes and client portfolios post positive returns for the first quarter, as you can see on your enclosed performance report.

Banking Update

The recent failures of Silicon Valley Bank, Signature Bank, and Credit Suisse are some of the largest bank failures in history. These failures, along with uncertainty regarding the solvency of approximately 300 other regional banks, created a lack of confidence in our banking system that added market volatility near the end of the quarter.

So what happened?

Multiple things led to the banks insolvency, but the primary issue was that many banks invested in long term bonds that lost significant value as the Fed pushed forth a quantitative tightening strategy whereby they increased rates an unprecedented 4.5% over just 12 months to try and cool off inflation. Regulators allow banks to report bond assets at par value if they are held to maturity, which seems reasonable, until there is a virtual instantaneous run on the bank in which those long-term bonds need to be sold to meet the withdrawal requirements. In SVB’s case the bank was 17 billion under water within a couple of days. Unable to meet their customers withdrawal requests and necessary reserve requirements, the banks become insolvent.

What’s next and should we be doing anything differently?

Although it has been inferred that all depositor accounts will be protected even beyond the FDIC limit of 250k, on March 12th the Federal Reserve also created a program that allows banks to meet any withdrawal obligations without having to sell their long-term bond holdings at a loss, before the bonds mature. This additional assurance helps the banking industry maintain a needed level of reliability to its customers and investors alike, by providing needed liquidity that will essentially come through the government at a low cost to help assure regional banks remain solvent. At this point the only recommendation we would make as it pertains to banking is to keep any of your banking accounts below the 250k FDIC amounts per account registration, as it seems prudent under the circumstances.

What impact will this have?

That is the key question, and it is a bit of a paradox. While the Fed has been doing everything it can to promote quantitative tightening (QT) by raising interest rates at a historically fast pace to curb inflation, now the Bank Term Funding Program (BTFP) has been established, which is actually a form of quantitative easing (QE) by infusing anywhere from 2 to 4 trillion of a new stimulus to help keep banks meet their obligations. How much the BTFP will need to back stop the banks remains to be seen but infusing that much more into our M2 money supply may counter the efforts to reduce inflation, thereby decreasing the value of the dollar and increasing inflationary pressures over the next couple of years.

The other impact of the recent banking crisis is that banks will likely be more conservative in their lending practices, which combined with the already higher interest rate environment may create a slower growth phase for the economy. Although the Fed is not projecting a recession, they have lowered GDP expectations to 0.5% for 2023 and less than 1.5% for 2024.

Economy

As you can see, much of the economic data remains strong when compared with the long-term averages for unemployment, job openings, corporate profits, and retail sales. However, it is clear that manufacturing, services, and consumer sentiment are waning, and the housing market continues its softening trend under the higher mortgage rate environment of approximately 6.5%. While we may be in for a period of slower growth, the one benefit of the Fed raising the Federal Funds rate to 5%, is that it now has a lever it can use to lower rates if they need to infuse dollars back into the system through rounds of QE in the future, which is something it didn’t have available when rates were at zero.

Market

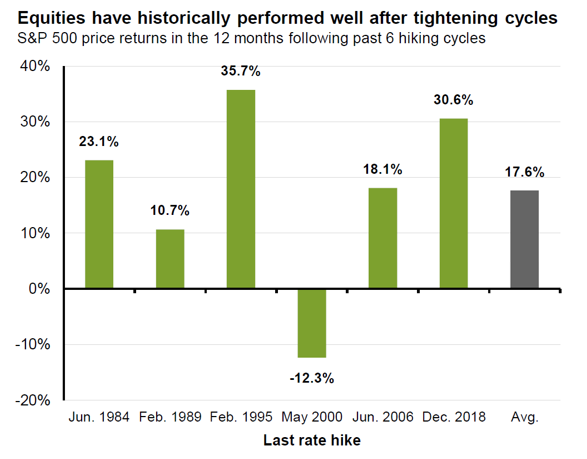

While markets have continued muddling through the last year with pressures from the Fed’s aggressive stance, war in Ukraine, political tensions and the banking crisis, we believe the pattern for growth moving forward will benefit higher quality companies with good liquidity and strong balance sheets. Based on PE ratios we believe the equity markets to be reasonably valued and that the bond markets will have a nice period of recovery once the Fed stops raising rates. As the Fed appears to be reaching their final rate increase, we found an interesting analysis from JP Morgan regarding 12-month market performance after the last Fed rate increase during a period of tightening.

Graph obtained from JP Morgan Weekly Market Recap as of March 27th, 2023.

As you can see on the graph above, over the last 40 years we have had 6 cycles of rate hiking, after which the market has provided average returns of 17.6%. Although past results are not a guarantee of future performance, it definitely helps build the case for holding the course through the uncertain times that follow periods of monetary tightening.

Portfolio

Enclosed is your most recent report on your portfolio. As you can see, while the longer-term numbers of our managers have been more encouraging, the last 12 months have definitely been a challenge. We continue to be encouraged with our individual managers’ relative performance vs. their indices, and believe maintaining our current style, sector, and asset class diversification is the most prudent approach as we look ahead.

Please take a few moments to review your enclosed report along with the enclosed copy of our privacy policy and updates to our ADV for your review. Should you have any questions or concerns, of course feel free to call. As always, we consider it an honor and privilege to work with you on your planning and look forward to doing so for many years to come.

Kindest personal regards,

Michael Brocker

MSFS, CLU, ChFC, AEP®, AIF®

Chartered Financial Consultant

Masters of Science in Financial Services

Matthew Brocker

MSFS, AEP®, RICP®, CAP®, AIF®

Masters of Science in Financial Services

Josh Brocker

CFP®, AIF®